The year 2020 saw digital camera shipments nosedive to a new low of 8.9 million units, down from 121 million units in 2010. It was believed it couldn’t get any worse and, indeed, shipments stabilized in 2021. So why do sales appear to be in free-fall again?

Looking back at camera shipments (which are different but closely related to sales) — as reported by CIPA — it’s actually not helpful to focus upon the number of units because it encompasses a wide swathe of different types of cameras.

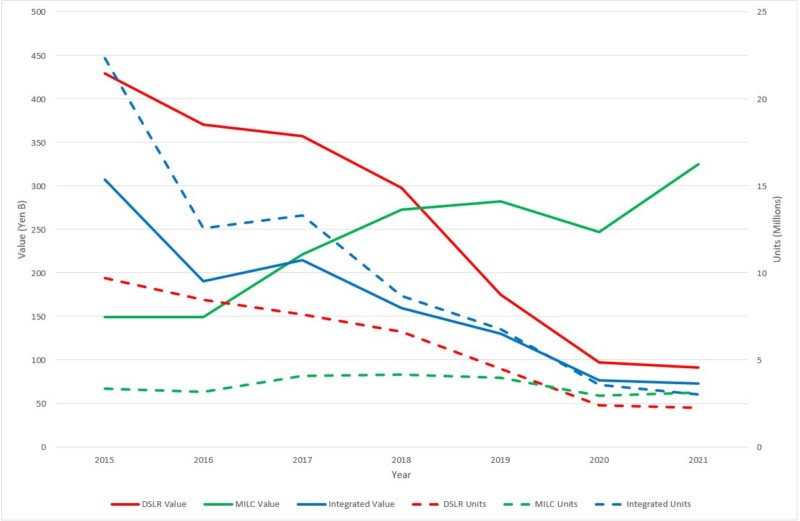

CIPA itself separates the sector into integrated, DSLR, and mirrorless types, recording both the number of shipments and their value. When you look at this, it’s clear that since 2014 integrated cameras (solid blue line) have ceased to be the financial driver for the industry; that mantle shifted to the DSLR (solid red line), as the figure below shows.

In fact, the picture is far more complex because the DSLR sector itself was in decline, just not disintegrating as fast as integrated-lens cameras. This is clearly demonstrated by the rise in the value of mirrorless shipments (solid green line) from 2016 onwards, even if more DSLRs were being shipped. By 2019 — a landmark year — mirrorless cameras were worth significantly more than DSLRs and by 2021 more were being shipped.

The message is clear: DSLRs are in terminal decline, with the volume and value of shipments now with mirrorless cameras. In addition, the demise of the integrated camera continues, shrinking inexorably into increasingly niche usage areas. Of course, these figures only outline the industry as a whole and don’t show the detail for individual manufacturers. 2016 was probably also a landmark year for mirrorless as it’s likely when Nikon and Canon finally realized they couldn’t stave off the inevitable march of Sony and had to join the club — and not in the half-hearted way that the EOS-M and System 1 lines did. It was a full-fledged pivot that saw both manufacturers release new, pro-oriented systems in 2018.

Since, Nikon had its own financial problems that have led it to focus almost exclusively on the Z-system, ramping down DSLR and integrated camera production. Canon had a bigger cushion to land on but is actually following the same path. Integrated cameras are being largely phased out and the EOS-M looks destined for the history books. Given that Canon and Nikon make up 90% of DSLR sales, it remains to be seen how long this segment will survive in any volume. If anything, COVID has sped up the decline of these two areas as it simply hasn’t been worth spinning production back up after factory shutdowns.

So, What is Happening In 2022?

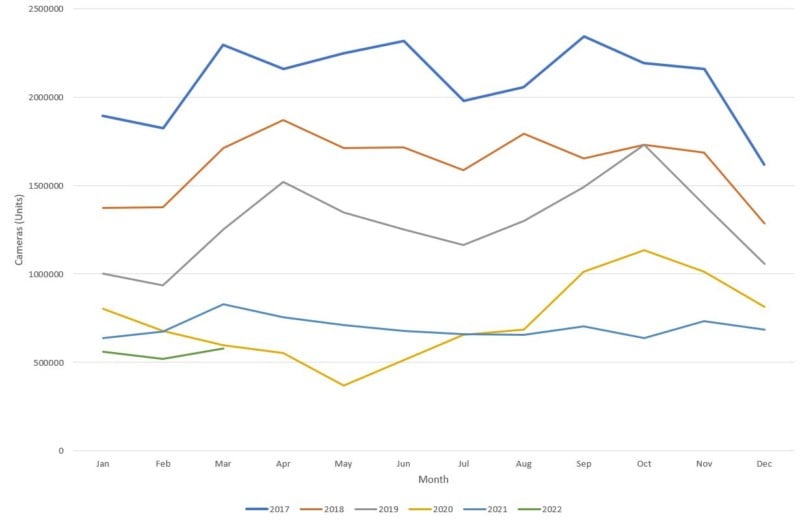

All that shows us how we got to the end of 2021, however business is about the future, not the past, and manufacturers will have broadly committed to a timetable of product design, release, and shipment for 2022 and beyond — notwithstanding problems related to COVID that affected production lines and the related supply of manufacturing parts. With the first quarter now complete, we can get a glimpse into how the year might shape up and it makes for some fairly grim reading on face value.

As the green line shows, it’s been a slow start to the year and the bump in shipments that normally comes in March just hasn’t happened. More than that, the healthy shipments from September, October, and November last year haven’t carried through.

The cumulative shipment total for the first quarter stands at 1.65 million, down from 2.14 million last year, which was down from 3.18 in 2019. What is worrying about that figure is that it has nearly halved from the pre-COVID levels. So where are the losses coming from?

Unequivocally they relate to a reduction in the number of integrated cameras shipping: some 3.01 million shipped last year, representing 36% of all models. That percentage is now standing at 26%, a big drop, with mirrorless up to 43% from 37%. Counter-intuitively, DSLRs are up to 31% from 27%, however, this will have no happy ending as that simply reflects that it isn’t performing as badly as the integrated camera category.

More pertinently, where is the money being made? Last year 66% came from mirrorless cameras and this now stands at 69%, with DSLRs dropping from 19% to 18% and integrated cameras from 15% to 13%.

Mirrorless cameras are where the money is in two ways: firstly, there are more units being shipped than for the other segments and, secondly, the unit value is significantly higher. In fact, the unit value of integrated models and DSLRs is about the same, and mirrorless is three times higher.

The latter reflects both the cost of new models (which are mirrorless) and that professionals and amateurs are buying into these systems. DSLRs remain a significant value segment where manufacturers can make money, but only by selling older models. There is clearly demand, but it’s diminishing.

Integrated cameras are an interesting segment because it’s changing from a low-cost, budget, item to a high value-proposition luxury good (such as the Sony RX100). So while the expectation is that integrated cameras will all but evaporate in 2022 — Canon is closing its principal Chinese camera factory and reducing shipments from 1.2 million to 0.67 million units — it will remain profitable in niche areas.

So what are the takeaways for the rest of the year? The first quarter is an excellent predictor of total shipments for the year, suggesting that manufacturers will hit 6.6 million units, down from 8.4 million last year. However, this reflects a manufacturer-driven reduction in integrated cameras and it seems likely that mirrorless units will be similar to, or will possibly exceed, the amounts from last year.

More than ever, both the volume and profit are being made in mirrorless which means manufacturers have to be both shipping and selling in order to be making a healthy income. Canon and Sony will be battling for those large shares, however all eyes will be on the fortunes of Nikon and Olympus. To a lesser extent, it will be interesting to see how many DSLRs ship. Will Nikon largely pull out of this segment? Will Canon expand its segment share and will Pentax be able to take advantage of its niche expertise? There is undoubtedly money to be made in the camera market, but it will take a keen eye and effective strategy to perform well.

Image credits: Header photo by Cole Keister, Unslpash.

Author: Mike Smith

Source: Petapixel